A simple interest formula is one of the most fundamental concepts in financial mathematics and, at the same time, one of the most used in the daily lives of companies and individuals.

Understanding how it works allows you to make more informed financial decisions, whether it's taking out a loan, analyzing a loan or negotiating payment terms.

In this article, you will understand what simple interest is, how to apply the formula correctly and in which situations this calculation model appears in business and personal practice.

What is simple interest?

Simple interest is the most basic way of earning capital over time. In this model, interest is always charged on the original amount invested or borrowed, the so-called initial capital, without the accumulated interest from previous periods being incorporated into the calculation base.

In other words, the amount of interest remains constant in each period, because the rate is always applied to the same amount.

This linear behavior differentiates simple interest from compound interest and makes it especially suitable for short-term operations, such as small loans, discounting trade bills and direct installment agreements between parties.

What is the simple interest formula?

A simple interest formula is expressed as follows:

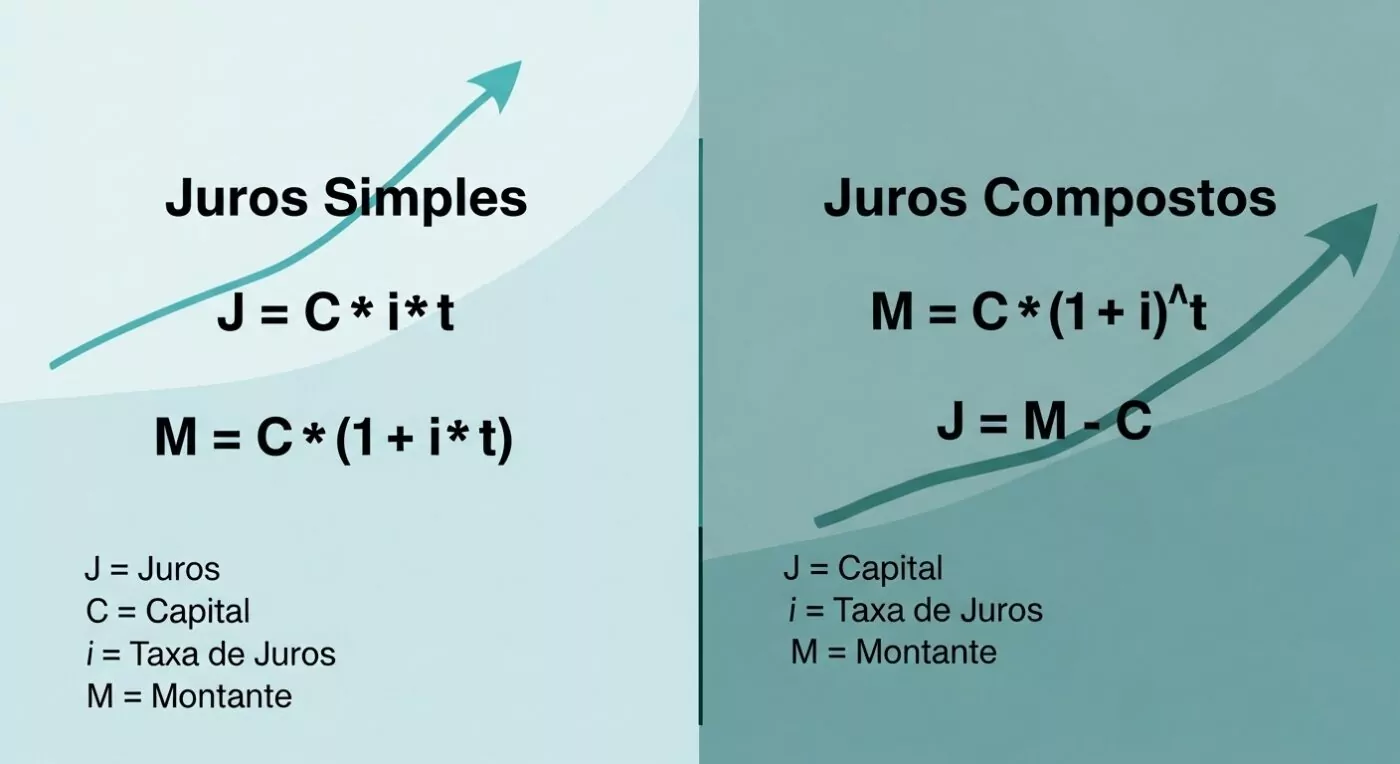

J = C × i × t

Where:

- J = interest value

- C = initial capital (amount borrowed or invested)

- i = interest rate (expressed in decimal or percentage, in the same period as t)

- t = time (application period)

To find the total amount at the end of the operation, use:

M = C × (1 + i × t)

The simple interest formula is straightforward: the value of the interest grows in proportion to the time and rate applied, with no capitalization effect. Therefore, doubling the term exactly doubles the amount of interest, something that doesn't happen with compound interest.

Ensuring a correct understanding of this formula is essential for interpreting contracts, pricing credit and assessing payment terms accurately.

What is the difference between simple interest and compound interest?

While simple interest formula keeps the calculation basis always fixed at the initial capital, the compound interest work differently: each period, the interest generated is incorporated into the capital, forming a new basis for the next calculation.

This mechanism, known as interest capitalization, causes the amount to grow exponentially in the compound system and linearly in the simple system.

In practice, for short periods and low rates, the difference between the two regimes is small. However, as time goes on, the gap between the values widens significantly.

A loan of R$ 10,000 at 3% per month for 12 months would generate R$ 3,600 in simple interest, but approximately R$ 4,258 in compound interest.

For this reason, the choice of interest regime directly influences the effective cost of a financial operation, and managers need to identify which model is being applied before signing any contract.

What simple interest is for

Simple interest is used to calculate the return on capital in short-term financial transactions with a linear structure.

In practice, this model is widely used in situations such as the discounting of bonds and bills, the calculation of fines for late payment, the monetary correction of debts and the pricing of informal loans between companies or individuals.

In addition, simple interest serves as a pedagogical basis for understanding more complex concepts of financial mathematics, such as compound interest and the internal rate of return.

For managers and entrepreneurs, mastering this calculation means having more clarity when analyzing credit proposals, negotiating with suppliers and evaluating contractual conditions.

Compare PF vs. PJ

with tax on dividends

What are interest rates?

The interest rate represents the percentage charged on a capital over a given period of time and it is precisely this that feeds the simple interest formula.

It can be expressed in different ways: per day, per month or per year, and must always be aligned with the unit of time used in the calculation. A rate of 2% per month applied for 6 months, for example, should be entered in the formula as 0.02, with the time equal to 6.

There are also important variations, such as the nominal rate, the effective rate and the real rate, the latter discounting the effect of inflation. Understanding these distinctions is fundamental to interpreting financial contracts accurately and avoiding surprises in the real cost of an operation.

How to calculate the simple interest rate

To calculate the simple interest rate, simply isolate the variable i in the main formula. The resulting expression is:

i = J ÷ (C × t)

In other words, the total amount of interest is divided by the product of the initial capital and the time. The result represents the rate per period, which can then be converted to a percentage by multiplying by 100.

This calculation is especially useful when you want to find out what rate is included in a credit proposal or installment plan.

Practical example with a rate of 2% per month:

Imagine that a company has taken out a loan of R$ 20,000 and will pay simple interest of 2% per month for 6 months.

Applying the formula:

J = C × i × t J = 20,000 × 0.02 × 6 J = 20,000 × 0.12 J = R$ 2,400

The total amount to be paid at the end of the 6 months will be:

M = C × (1 + i × t) M = 20,000 × (1 + 0.12) M = 20,000 × 1.12 M = R$ 22,400

In this scenario, the company will pay R$ 2,400 in interest on the R$ 20,000 taken out, totaling R$ 22,400 at the end of the period. Note that, as we are using the simple system, the R$ 400 generated each month remains constant from start to finish, there is no capitalization.

Where simple interest is applied

Simple interest rates appear in various situations in the financial and business environment. In the credit market, they are common in short-term operations, such as personal loans with a term of up to 12 months and working capital financing.

In the fiscal and tax context, fines for late payment of federal taxes, These are often calculated on the basis of the Selic rate, and often follow the simple regime for specific periods.

Commercial discounting of trade bills and post-dated checks also uses this model. In negotiations between companies, agreements to pay debts in installments with suppliers or customers usually use simple interest because of the transparency and ease of verifying the amounts involved.

How to find out the capital at simple interest

In some situations, the manager knows the final amount, the rate and the term, but needs to find out what the initial capital of the operation was. To do this, simply reorganize the simple interest formula and isolate the C:

C = M ÷ (1 + i × t)

This calculation is especially useful when discounting receivables, when a company advances a bond and wants to know the net amount it will receive after deducting interest.

For example: if the amount of a bond is R$ 15,000, the rate is 1.5% per month and the term is 4 months, the present capital will be R$ 15,000 ÷ 1.06, resulting in approximately R$ 14,150.

Knowing about this inverse operation increases the manager's analytical capacity when faced with proposals to advance receivables and factoring operations.

How to use the simple interest formula in your company

Apply the simple interest formula in day-to-day business goes far beyond solving mathematical exercises, it is a concrete financial management tool.

A manager can use it to assess whether the conditions of a loan are advantageous, compare proposals from different financial institutions, calculate the real cost of an installment plan with suppliers or price installment sales in such a way that the margin is not eroded by embedded interest.

The formula helps to identify inconsistencies in contractsWhen the reported rate does not match the amounts charged over time, this may indicate that the regime applied is the compound one and not the simple one as advertised.

Another important use is in default analysis: calculating charges for late payments based on a contractually defined rate and term requires exactly this mastery.

Companies that incorporate this type of thinking into their financial routine make more informed decisions, reduce unnecessary costs and negotiate with much more certainty.

Count on CLM Controller to calculate your company's interest payments

Understanding the simple interest formula is the first step, but applying it correctly within a company's financial reality requires expertise, context and strategic vision.

This is where CLM Controller makes the difference. With more than 40 years of experience and a team of more than 100 specialists, CLM offers much more than traditional accounting services: it delivers financial intelligence applied to the client's business.

Through services such as Financial Management, Financial BPO, Tax consultancy e CFO as a Service, CLM helps entrepreneurs and managers interpret credit operations, analyze financial charges, optimize cash flow and make decisions based on accurate data.

{kind=link}

Each client has an exclusive account manager, with a consultative and strategic approach, ensuring that no financial detail goes unnoticed.

If your company operates on Real or Presumed Profit and needs accounting that goes beyond compliance with obligations, talk to an expert of CLM Controller and request a strategic diagnosis for your business.

Upgrade your finances:

Talk to us!