In this episode, Marco Aurélio talks to Rodrigo Ribeiro, director of CLM Controller, This is a question that is increasingly common among entrepreneurs and professionals: at what point does the higher profitability of the individual compensate for the tax paid on the withdrawal of profits from the company?.

From 2026, the profits and dividends distributed partners will receive 10% withholding tax.

This change makes many entrepreneurs wonder: is it worth withdrawing funds from legal entities to invest in individuals despite this initial tax?

In this article, we use a practical example to show in how many years the higher profitability as an individual can offset the so-called “toll” of dividend tax.

Simulation assumptions

To simplify the analysis, we have adopted the following realistic assumptions:

-

Amount available in PJ: R$ 100,000

-

Tax rate on dividends (from 2026): 10%

-

Annual gross return on investment: 10% p.a.

-

Taxation on financial income: 15% for individuals and 34% for companies (IRPJ+CSLL)

-

Reinvestment of earnings: all interest is reinvested annually

-

Analysis horizon: long term (several years)

Compare PF vs. PJ

with tax on dividends

Initial cost of the decision (the “toll”)

Withdrawing R$100,000 from the company in 2026 causes a tax of 10%, i.e. R$10,000 payable at source. The table below summarizes this initial “toll”:

| Description | Value |

|---|---|

| Amount distributed | R$ 100,000 |

| Tax (10%) | R$ 10,000 |

| Net capital | R$ 90,000 |

After pay the tax, This leaves R$90,000 to invest in the individual. This cost of R$10,000 needs to be recovered through the difference in net profitability over time.

Comparison of net profitability

With the rates defined, the net annual return on each investment is:

-

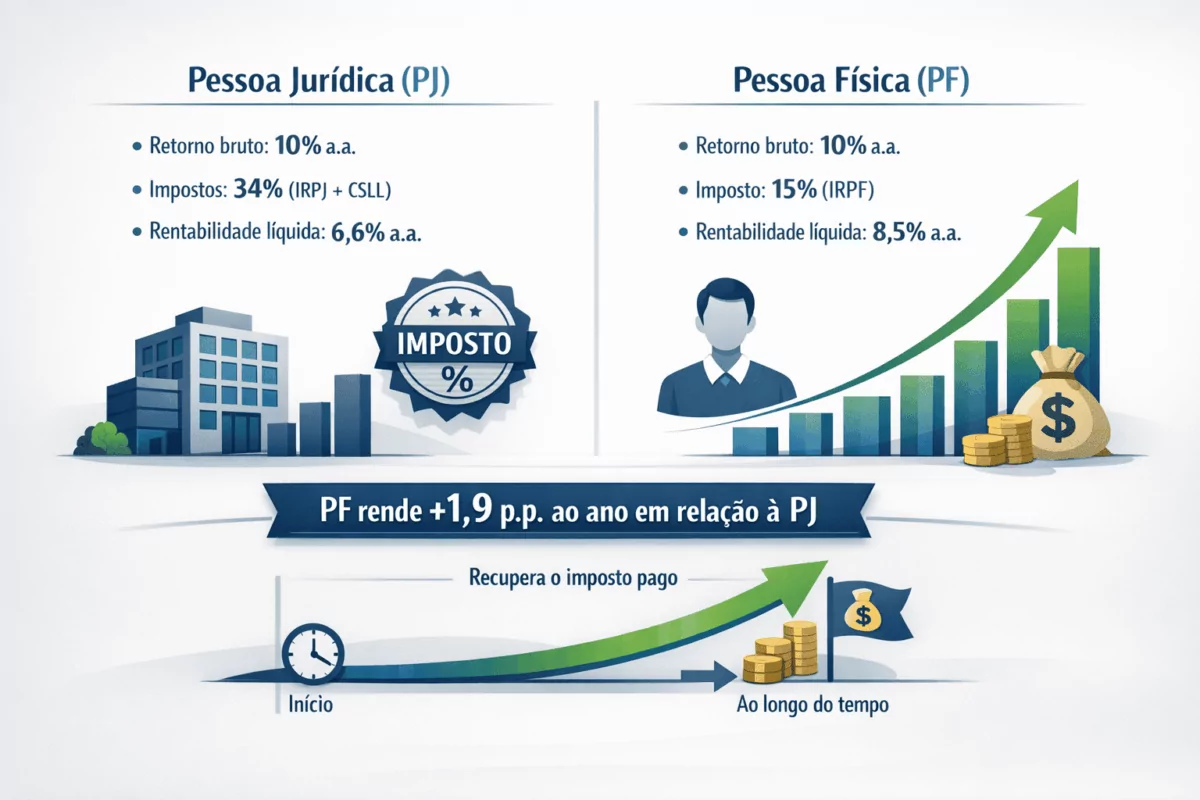

Legal entity (PJ): gross return of 10% p.a., minus 34% of tax (IRPJ+CSLL), results in around 6.6% p.a. liquid.

-

Individual (PF): gross return of 10% p.a., minus 15% tax (IRPF), results in about 8.5% p.a. liquid.

In practical terms, investing as a PF yields 1.9 percentage points per year more than reinvesting in the PJ. This annual difference (8.5% vs 6.6%) will be the “force” that makes the individual recover the initial tax paid.

Evolution of assets over time

Considering the above net returns, we project the future value of the investments over a few years:

| Time | PJ (6.6% p.a.) | PF (8.5% p.a.) |

|---|---|---|

| 5 years | R$ 137.653 | R$ 135.329 |

| 6 years | R$ 146.738 | R$ 146.832 |

| 7 years | R$ 156.423 | R$ 159.313 |

| 8 years | R$ 166.747 | R$ 172.854 |

It can be seen that around the age of 5, the values become almost the same. At 6th grade, The amount invested as a PF exceeds that of the PJ (R$146.832 > R$146.738). This is the break-even pointFrom then on, the balance in the PF recovers the tax paid and begins to earn more than it would have invested in the company.

New exemption calculator

IR

It's worth transferring to the PF if:

-

the money can be invested for 6 years or more;

-

is part of long-term equity reserves (not used in the company's operations);

-

the focus is on accumulating wealth.

It may not be worth it if:

-

there is a need to reinvest resources in the company in the short term;

-

the horizon for using the money is short (up to 4-5 years);

-

the capital is used as the company's operating turnover.

Each case must take into account the term and purpose of the resource. Transferring to a PF makes sense when the investment is long-term and the entrepreneur doesn't need the capital for immediate operations. Otherwise, it may be more advantageous to keep the funds in the PJ, especially in the short term.

Your money can earn more

invest with Diagrama l XP

Pocket rule for deciding

-

Horizon > 6 years: PF tends to overtake PJ.

-

Horizon < 5 years: PJ might make more sense.

-

Between 5 and 6 years old: gray area (depending on the actual profitability achieved).

This simplified rule helps guide quick decisions: a long time horizon favors the individual, short terms favor leaving resources in the company.

Do you have any questions about the taxation of profits? Talk to us

Conclusion

The example shows that the decision to withdraw resources from the company is not only tax-related, but also strategic. The “entry fee” of 10% in dividend tax is only amortized over the medium term. Thinking only about the initial tax (the toll) can lead to wrong decisions. Those who focus on future cash flow in other words, in net returns over time, you tend to get your planning right. Therefore, evaluating the investment horizon and the use of capital is essential when deciding between PJ and PF.

About CLM Controller

O CLM Controller is a firm specializing in tax planning and equity for companies and partners. We have expertise in simulating scenarios and analyzing results to support strategic decisions. Our team helps entrepreneurs design alternatives such as withdrawing dividends, evaluating scenarios and tax impacts to guide the best long-term actions.

Tax outsourcing

The strategic solution for companies