2026 marks an important change in the Simples Nacional. The 2025 Tax Reform introduced new rules that directly affect micro and small companies opting for the regime. From now on, the IRS will analyze the economic reality of the business, and not just the formal documents or contracts.

In other words, it's not enough to have separate CNPJs on paper, but if the companies operate as a single business in practice, this will be taken into account. Two central points deserve special attention: the new concept of economic group and the expanded definition of gross revenue in Simples.

What will change in Simples Nacional from 2026?

Complementary Law 214/2025 (part of the Tax Reform) brought adaptations to Simples Nacional, without extinguishing the regime, but changing some internal rules. Two changes stand out:

-

Stricter and more digital supervision: A Receita Federal has integrated systems and data with states and municipalities, allowing electronic cross-checks in real time.

-

Combating the fragmentation of companies: Combating the fragmentation of companies: There were cases of entrepreneurs opening several companies in order to fragment their turnover and thus pay less tax or remain in Simples unduly. As of 2026, the tax authorities are keeping a close eye on this practice. The aim is to prevent the same business from being artificially divided into several CNPJs just to take advantage of lower taxation.

In short, from 2026 the government will continue to encourage small businesses with Simples, but with more control. The changes in Tax reform have integrated Simples Nacional into the new consumption tax system (IBS/CBS), but without changing the rates - what has changed is the way billing is calculated and monitored.

Complete Guide to

Tax reform

Economic group: what is considered

One of the most impactful changes is the new understanding of economic group, This is a de facto and de jure group. In simple terms, an economic group is when two or more companies, although each has its own CNPJ and formal autonomy, are under common control or management or act as if they were a single business unit. It doesn't just matter about the contract company or corporate structure - what counts is how companies work in practice.

The IRS now looks at various elements to identify a de facto economic group:

-

Common control: Companies that have the same owners, related partners (family members) or a partner who has power over all of them. For example, if you and your spouse own several companies, this already indicates shared control.

-

Integrated economic action: Companies that operate in a complementary or coordinated manner, presenting a steering unit and common goals. For example, one company produces and another sells the same products, or they share customers and suppliers strategically.

-

Common interests: When companies aim for the same economic result, acting together rather than competing. If the success of one depends on the other, there is a sharing of interests.

-

Structure sharing: Joint use of office space, stock, equipment, brand or employees by theoretically separate companies. For example, two separately registered companies work at the same address and share the same staff, with no clear separation of expenses.

-

Asset and financial confusion: Mixing of resources and assets between companies. For example, one company pays bills or salaries that would have belonged to another, or they all use assets that belong only to an individual linked to the group. In a real case, several companies were excluded from Simples because they used the same buildings and employees, There was no official division of costs - in other words, they operated as departments of a single company.

Economic group: what is considered

One of the most impactful changes is the new understanding of economic group, This is a de facto and de jure group. In simple terms, an economic group is when two or more companies, although each has its own CNPJ and formal autonomy, are under common control or management or act as if they were a single business unit. It doesn't just matter about the articles of association or the corporate structure - what counts is how companies work in practice.

The IRS now looks at various elements to identify a de facto economic group:

Read also: Rearp, the legal chance to adjust your assets and reduce future taxes

-

Common control: Companies that have the same owners, related partners (family members) or one partner with power over all of them.

-

Integrated economic action: Companies that operate in a complementary or coordinated manner, presenting a steering unit and common goals.

-

Common interests: When companies aim for the same economic result, acting together rather than competing. If the success of one depends on the other, there is a sharing of interests.

-

Structure sharing: Joint use of office space, stock, equipment, brand or employees by theoretically separate companies.

-

Asset and financial confusion: Mixing of resources and assets between companies. For example, one company pays bills or salaries that would belong to another, or they all use assets that belong only to an individual linked to the group.

These factors characterize the de facto economic group, even if there is no formal contract linking the companies. If two or more companies have unified management and operation, If the legal entities are separated merely on paper, it is considered that there has been an artificial separation of legal personalities. In other words, for inspection purposes, several companies can be treated as one when there is this unity of command and lack of real independence.

Important: economic group of law is one that is formally recognized (for example, a holding company controlling subsidiaries). The economic group in fact is identified by the context of the operations, even without explicit corporate ties.

The IRS now pays special attention to de facto groups. Having separate articles of association is not enough - if the companies operate as a single business, the tax authorities can classify them together.

Maximize your benefits with

Holdings

What really changes in practice in 2026

To visualize the changes, let's look at a simple comparison of the situation before e after 2026:

| Criteria | Until 2025 (Previous Scenario) | From 2026 (New Reality) |

| Integration | Individual bodies (Union, States, Municipalities). | Unified data and real-time cross-checking. |

| Statements | For information purposes only (PGDAS/DEFIS). | Confession of debtautomatic charging. |

| Penalties | Slow and reactive enforcement. | Immediate fines for errors or omissions. |

| Groups/Members | Manual identification of linked companies. | Consolidated turnover via algorithm. |

In short, in the day-to-day practice of the entrepreneur, 2026 brings less room for error or “jeitinho”. Everything has become more transparent and digitally connected: if before some informality went unnoticed, now the system automatically cross-references invoices, bank transactions and statements from different sources. Therefore, extra attention must be paid to the organization and veracity of the information provided.

Direct impacts for those in Simples

What are the risks and impacts of these changes for small Simples Nacional companies? Let's break down the main ones:

1. The “Global Ceiling” of R$ 4.8 Million

Having several CNPJs to “spread” the billing no longer works. If the system detects that the companies operate as an economic group (same partners, addresses or structure), the billing is added. If the sum exceeds the limit, they are all excluded from Simples at the same time.

2. The Boomerang Effect (Retroactivity)

Disqualification is not just for the future. If the irregularity is detected in 2026, the IRS can go back to 2025 or earlier, demanding the difference in taxes for the entire period as if the company had never been a Simples member.

3. The Risk of Fatal Liabilities

The retroactive charge is accompanied by:

-

Difference in rates: (e.g. from 10% in Simples to 34% in Lucro Presumido/Real).

-

Heavy fines: They can reach 150% in cases of fraud or collusion.

-

SELIC interest: Accumulated over the entire period.

This accumulated amount has the potential to make the business financially unviable overnight.

4. Joint and several liability (shared debt)

If it is proven that “asset confusion” (the money of one company pays the bills of the other or of the partners without discretion), the IRS can collect the debt of a CNPJ directly from the cash of the other companies in the group or from the personal assets of the partners.

5. Substance over Form

The CNPJ number is just a record. What the tax authorities now validate is the actual operation. If the companies are not genuinely independent (with separate employees, headquarters and operations), the risk of them being considered a single unit is extremely high.

In 2026, tax savings based on “divide and conquer” became the most dangerous strategy for a company. The focus must shift to operational efficiency and legal tax planning in regimes such as Presumed or Real Profit, if growth exceeds the ceiling.

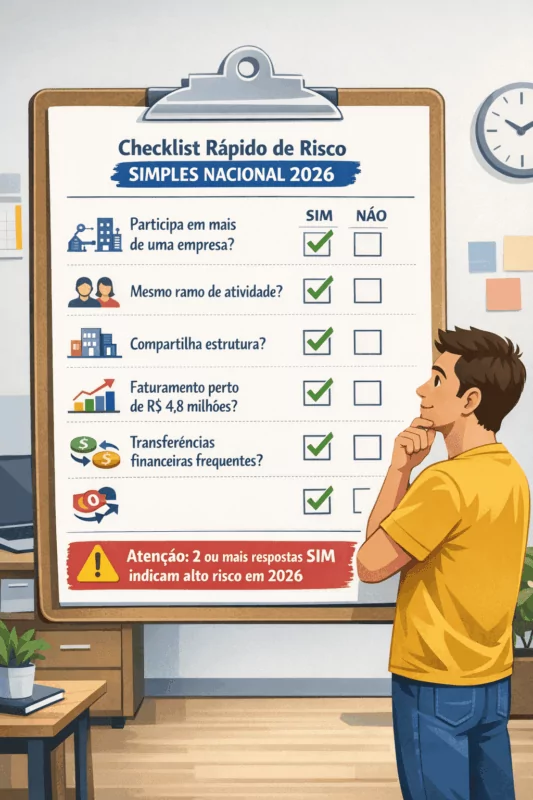

Rapid risk checklist (2026)

In order for small entrepreneurs to assess whether they may be at risk under the new rules, we have prepared a simple checklist for YES or NO. Answer the questions below objectively:

-

Do you (or your partners) have a stake in more than one Simples Nacional company? - (Yes/No)

-

Do these companies operate in the same line of business or in complementary activities? - (Yes/No)

-

Do the companies share an address, physical structure, employees or equipment? - (Yes/No)

- Are the sales or services of one company mainly destined for customers or suppliers of the other? - (Yes/No)

-

Is the combined turnover of the companies close to or over R$ 4.8 million per year? - (Yes/No)

-

Do companies frequently make financial transfers to each other (loans, paying bills) without clear formal contracts? - (Yes/No).

If you answered “YES” to two or more of the above questions, a high-risk alert goes off. This indicates that your companies could be viewed as an economic group by the IRS in 2026. It's worth going to your accountant and reviewing the situation.

To understand how the 2026 changes will impact your company and avoid tax risks, count on a specialized tax consultancy. A CLM Controller helps you organize the structure of your business, maintain compliance with Simples Nacional and make safe decisions, with planning and strategic vision.

New concept of gross revenue in Simples Nacional

What has changed in Simples billing?

How it was before

You basically paid tax on direct sales of products or services that were part of their corporate contract (CNAE). Other “secondary” cash inflows were often left out of the calculation.

How it is now (2026)

The rule has become broader. Now, everything that comes from your company's operations counts as turnover for tax purposes, even if it is not your main activity.

What goes on the tax bill now:

-

Interest on installments: If you charge your customer interest because they paid in installments, that interest is now billing.

-

Tips: For bars and restaurants, tips (even spontaneous ones) are now part of the company's turnover.

-

Rents and Royalties: If you rent equipment or space in connection with your business.

-

Sponsorship: Money received to carry out company events or actions.

-

Services “outside” the CNAE: Any income linked to the business, even if you forgot to put the specific activity code (CNAE) in the contract.

What remains OUT (does not pay Simple):

-

Sale of company assets: Did you sell a car or a machine that belonged to the company? The profit from that doesn't go into Simples.

-

Bank income: The interest that your company's money earns in your bank account or in investments.

-

Compensation: Money received from insurance for a claim.

The two big risks to your pocket

-

Indirect tax increase: The tax rate (the percentage) hasn't changed, but as you now add more things to your turnover, the final amount of your tax bill (DAS) may be higher than before.

-

Risk of exclusion from Simples: If your company's turnover is close to the R$ 4.8 million per year, Beware! These “extra revenues” (such as tips or interest) can cause you to exceed the ceiling and be forced to leave Simples Nacional, moving to Lucro Presumido or Real, where the tax is usually much higher.

Spreadsheet

Simples taxes

Comparative table: gross revenue before vs after 2026

To help you understand, see the table below for a comparison of the concept of gross revenue before e after of change:

| What is evaluated | Old Rule (Until 2024) | New Rule (2025/2026) |

| Main focus | Only what was in your CNAE (official paperwork). | Everything that comes in from the operation of the business. |

| Extra income | Interest on installments and tips were often left out. | They are included in the bill. Interest, tips and rents now pay tax. |

| Secondary activities | If it wasn't in the articles of association, many people wouldn't declare it. | Even if it's not in the contract, If the money came from the business, it is taxed. |

| What has NOT changed | Sale of assets (furniture/cars) and profit from bank investments were out. | They're still out. Investments and the sale of company assets do not pay Simples. |

(Note: “Since 2025/2026” - the Law came into force in 2025, but many will only feel the practical effects in 2026, when there is consolidation of annual turnover and more active inspection).

In short, the Simples company must now consider all sources of income related to your business when calculating your taxes. This change requires greater attention when registering entries: something that might previously have been entered “outside” the invoice now needs to be officially recorded.

What to do preventively

Faced with so many changes, what can (and should) small entrepreneurs do to prepare and avoid problems with the IRS? Below is a list of checklist of practical actions and preventive measures:

1. Paperwork vs. Reality (CNAE)

There's no point in your articles of association saying one thing if the money coming in comes from another.

-

Action: Check that your company's activity codes (CNAEs) match what you actually sell. If you've started providing a new service, update the contract. The government now taxes what you does, not just what is written.

2. No “All Together and Mixed”

If you have more than one company or common partners, you should be doubly careful.

-

Action: Keep bank accounts, employees and addresses separate. If one company uses the other's equipment, make a rental agreement formal. Paying the electricity bill of “Company A” with the money of “Company B” without a document is a serious mistake that can lead to exclusion from Simples.

3. Divide expenses officially

Does your administrative structure serve two different CNPJs?

-

Action: Create a apportionment contract (division of costs). Document exactly how much each company pays for the office or shared desk. This proves that there is no confusion of money between the companies.

4. Keep an eye on the R$ 4.8 million limit

As almost everything now counts as turnover (interest, tips, etc.), you can reach the Simples ceiling much more quickly.

-

Action: Ask your accountant for a monthly report on your accumulated turnover. Don't wait until December to find out that you've exceeded the limit; if you have several companies with the same partners, add up the turnover of all to see if it's still safe.

5. Have a “Plan B” (Tax Planning)

Sometimes, growing within Simples becomes too expensive or risky with the new rules.

-

Action: Ask your accountant if it's worth migrating to the Presumed Profit or Real Profit. Planning to leave Simples in an organized way is much cheaper than being expelled by the government and having to pay back taxes with a fine.

Conclusion

In summary, the changes to Simples Nacional from 2026 onwards do not mean a tax increase, but a tightening of the rules to ensure that each company collects taxes according to its economic reality. The tax rates remain the same and no new taxes have been created. The main point of attention for the small entrepreneur is the way the business is organized, since artificial structures, undue fragmentation or lack of transparency will be identified much more quickly by the IRS.

In this scenario, planning and expert guidance are no longer differentials, but essential. This is precisely where CLM Controller acts strategically, helping companies assess risks, review corporate structures, organize billing and keep their operations fully aligned with Simples Nacional rules. The aim is not just to avoid tax problems, but to guarantee security, predictability and peace of mind for business growth.

Upgrade your finances:

Talk to us!