Choose between Simples Nacional or Presumed Profit It is one of the most important tax decisions any company can make.

An inappropriate tax structure can increase the tax burden, compromise cash flow, and reduce the business’s competitiveness. On the other hand, a decision based on a comprehensive tax assessment can result in annual savings of tens or even hundreds of thousands of reais.

That decision became even more strategic in 2026. With the changes brought about by Tax reform and the start of the implementation of the Dual VAT (CBS and IBS), many companies have begun to reassess their tax structures.

In this comprehensive guide, you’ll learn about the main differences between Simples Nacional and Lucro Presumido, how taxation works under each system, what factors to consider before switching, and in which situations it’s worth changing tax systems.

What is Simples Nacional?

O Simples Nacional It is a tax system designed to simplify tax collection from micro and small businesses. Under this system, various federal, state, and municipal taxes are paid using a single payment form, known as DAS (Simples Nacional Collection Document).

Companies with annual gross revenue of up to R$ 4.8 million, provided they meet the other requirements set forth in the law.

Taxes typically included in the DAS include:

- IRPJ;

- CSLL;

- PIS;

- Cofins;

- IPI (when applicable);

- CPP (except for companies listed in Annex IV);

- ICMS;

The main advantage of Simples Nacional is precisely its operational simplicity. In addition to consolidating tax payments, the system reduces ancillary obligations compared to other tax systems.

However, simplicity does not necessarily mean a lower tax burden. This is one of the biggest misconceptions found in companies.

Many business owners remain in the Simples Nacional program for years without realizing that another tax regime could offer much greater savings.

How does the Simples Nacional tax system work?

Contrary to what many people think, the Simples Nacional There is no single tax rate. Taxation depends on several factors:

- Occupation;

- Tax Schedule;

- Total revenue for the past twelve months;

- R Factor (for certain activities).

Today, the system is divided into five schedules, each with its own revenue brackets and tax rates.

That's why two companies with the same revenue They may collect their taxes at completely different rates.

A technology company, for example, may be taxed under Annex III or Annex V, depending on the R Factor. A construction company, on the other hand, will be subject to Annex IV.

This complexity shows that Simples Nacional is no longer a “simple” system from a strategic standpoint.

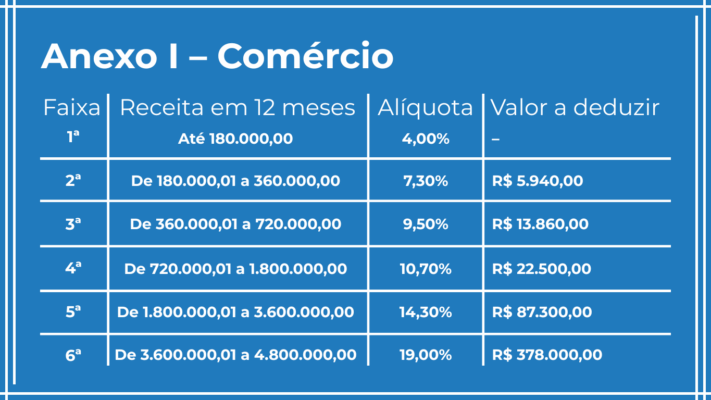

Annex I – Trade

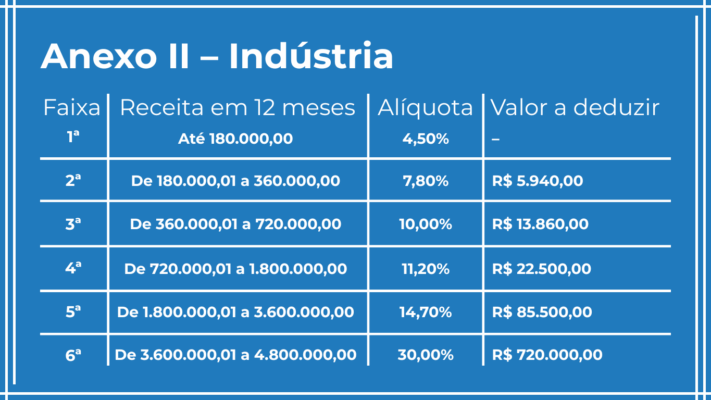

Annex II – Industry

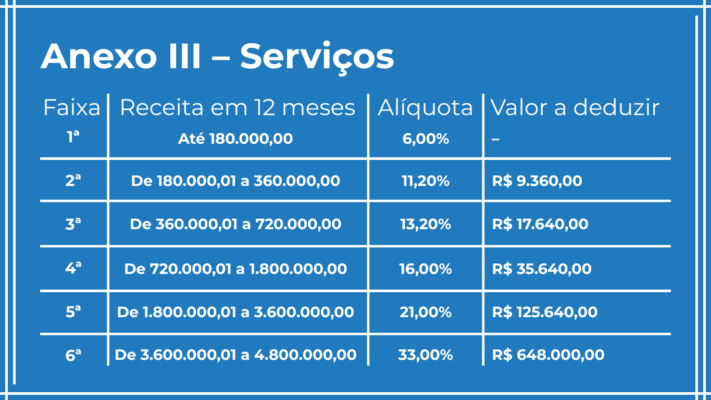

Annex III – Services

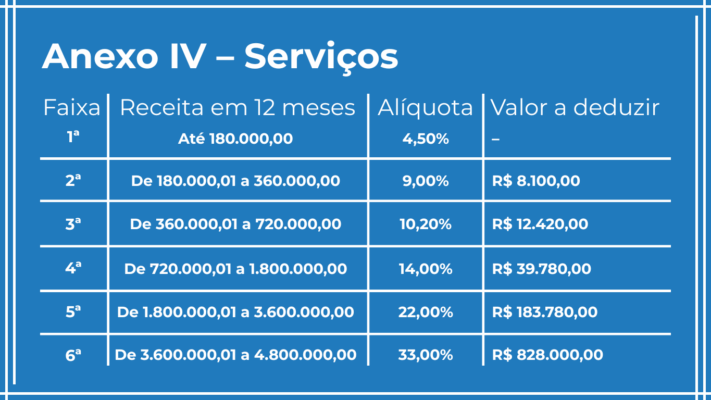

Annex IV – Services

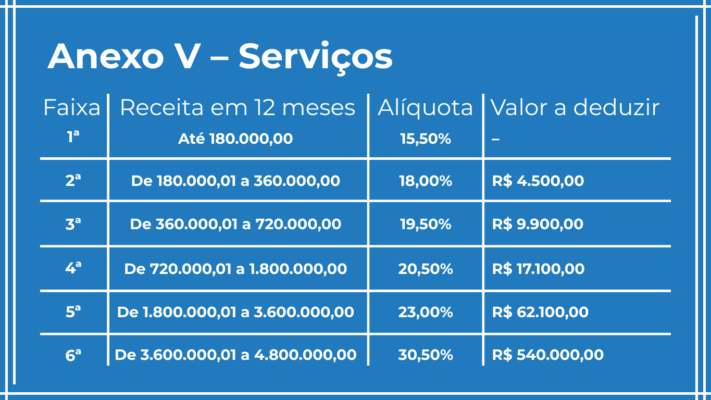

Annex V – Services

That said, we need to clarify that considering the values in the "Deductible amount", The maximum effective Simples Nacional tax rate is 19.50% on monthly turnover.

Spreadsheet

Simples taxes

What is Presumed Profit?

O Presumed Profit It is a tax system in which the law presumes a profit margin on the company's revenue to calculate part of its federal taxes.

Instead of calculating the actual profit earned, the law establishes presumptive percentages based on the type of economic activity.

These percentages serve as the basis for calculating:

- IRPJ;

- CSLL.

However, taxes such as:

- PIS;

- Cofins;

- ISS;

- ICMS (when applicable)

They continue to be calculated according to their own rules.

The Presumed Profit method is commonly used by service providers, medical clinics, consulting firms, holding companies, technology companies, and various medium-sized businesses.

Although it is more complex to administer than Simples Nacional, It also offers significant tax planning opportunities.

How does Presumed Profit taxation work?

One of the main differences lies precisely in how taxes are calculated. While under the Simples Nacional system virtually all taxes are paid on a single payment slip, under the Presumed Profit system each tax has its own method of calculation.

The main taxes are:

- IRPJ;

- CSLL;

- PIS;

- Cofins;

- ISS;

- ICMS (when applicable);

- Payroll tax.

This separation requires more robust accounting and tax controls. On the other hand, it allows for a tax planning much more flexible.

Depending on the company's structure, this flexibility can result in significant savings.

IRPJ

In Presumed Profit, we need to multiply one of the rates below by the 15% rate of IRPJto arrive at the percentage that will be applied to turnover to calculate the tax due.

Thus, a company that sells goods will pay 8% x 15% = 1.20% of IRPJ on turnover.

| Activities | Rate |

| Retail sale of fuel and natural gas | 1.60% |

| - Sale of goods or products - Cargo transportation - Real estate activities - Hospital services - Rural Activity - Industrialization with materials supplied by the ordering party - Other unspecified activities (except provision of services) | 8 % |

| - Transportation services (except freight) - General services with gross revenue up to R$ 120,000/year | 16% |

| - Professional services - Business intermediation - Management, leasing or assignment of movable/immovable property or rights - Services in general, for which no specific percentage has been set | 32% |

CSLL

In turn, to calculate the CSLLIn order to calculate the tax due, we need to multiply one of the rates below by the 9% rate, and only then arrive at the percentage that will be applied to the turnover to calculate the tax due.

Therefore, a company that sells goods will pay 12% x 9% = 1.08% of CSLL on turnover.

| Activities | Rate |

| Trade Industry Hospital services Transportation services | 12% |

| Services in general, except hospital and transportation services Business intermediation; Management, leasing or assignment of real estate, furniture and rights of any kind. | 32% |

PIS and COFINS

In the case of PIS and COFINS, In this case, we should use the following calculation rates on turnover:

- PIS: 0.65% on turnover;

- COFINS: 3% on turnover.

ICMS and ISS

Finally, the ICMS and ISS are calculated based on the rates and what is determined by state legislation (in the case of ICMS) and municipal legislation (in the case of ISS).

Having made this comparison, the question remains: when should you migrate from Simples Nacional to Lucro Presumido? The answer is in the next article.

Spreadsheet

Presumed Profit

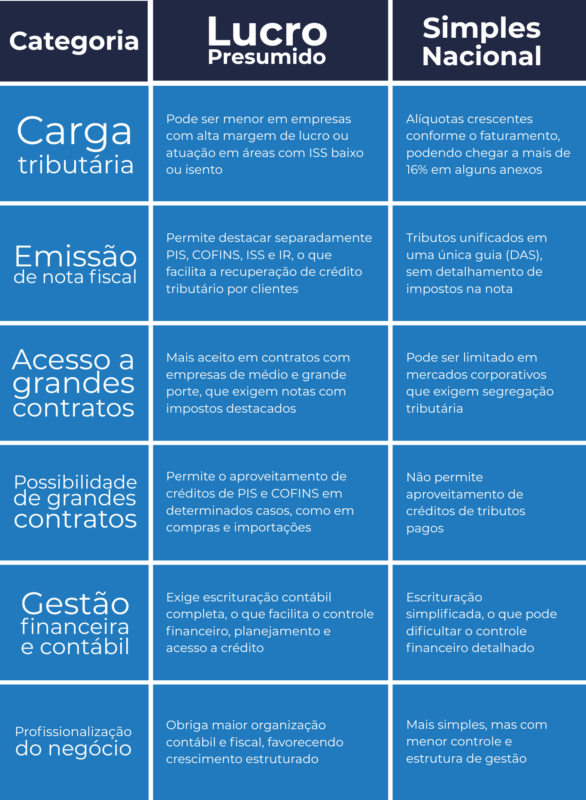

Comparison: Simples Nacional vs. Presumed Profit

In Simples Nacional, taxation is based on an effective tax rate calculated according to the company’s cumulative revenue over the past 12 months and the tax bracket to which the company belongs.

In Presumed Profit, each tax is calculated separately. The final percentage depends on the type of business activity, the municipality (ISS), the ICMS tax rate when applicable, and the payroll.

Here's a simplified comparison:

Aspect | Simples Nacional | Presumed Profit |

Revenue Limit | Up to R$ 4.8 million/year | Up to R$ 78 million/year |

Method of collection | Single entry form (DAS) | Taxes Collected Separately |

Initial tax rate | Starting at 4% (retail), 4.5% (manufacturing), and 6% (services), as shown in the appendix | There is no single tax rate; taxes are calculated individually |

IRPJ | Included in the DAS | Presumed tax base of 8% (commerce/industry) or 32% (most services), on which 15% of IRPJ is levied, in addition to the surcharge when applicable |

CSLL | Included in the DAS | Presumed base of 12% (commerce/industry) or 32% (services), on which a tax rate of 9% is applied |

PIS/Cofins | Included in the DAS | Cumulative tax regime: 0.65% for PIS and 3% for Cofins on gross revenue |

ISS and ICMS | Included in the DAS for service providers | Collected separately, in accordance with the rules and rates set forth in local law. |

CPP (Employer's INSS) | Included in the DAS for companies listed in Annexes I, II, III, and V; reported separately in Annex IV | Collected separately from payroll |

This table shows that the decision should not be based solely on operational convenience. Growing companies typically need to evaluate much broader factors.

In many cases, companies remain in the Simples tax regime simply because they have never filed a comprehensive tax assessment.

Over the years, revenue grows, the operational structure changes, the customer base evolves, and the tax regime ceases to be the most efficient. Even so, no review is conducted.

The result is often a higher tax burden than necessary. It is precisely at this point that a Technical analysis starts to make a difference.

Simples Nacional or Presumed Profit: A Comparison by Business Type

So far, it has become clear that there is no single tax system that is universally better. The choice depends on the characteristics of the company.

With that in mind, let's analyze how this decision impacts different segments and what criteria a CFO you should consider before choosing between Simples Nacional and Presumed Profit.

Technology Companies: Is Simples Nacional Still the Best Option?

Startups, software companies, systems development firms, IT consulting firms, SaaS solution providers, and cybersecurity companies They usually start out under the Simples Nacional system because of its simplicity and, in many cases, the reduced tax burden.

However, as these companies grow, the landscape changes.

Imagine a software company that had annual revenue of R$ 800 mil and, after winning new contracts, began generating annual revenue of R$ 4 milhões.

In addition to the increase in the effective tax rate under the Simples Nacional system, other factors now directly influence the decision, such as:

- Payroll growth;

- Composition of the customer base;

- Contracts with large companies;

- The need to use tax credits;

- Expansion into other states;

- Corporate planning.

It is common for technology companies to serve large corporate clients. In such cases, tax considerations no longer affect only the service provider but also have an impact on the client.

With the gradual implementation of the Tax reform, this analysis has become even more relevant.

Companies under the Presumed Profit regime may offer greater tax efficiency in B2B transactions, especially when their customers value the use of credits.

However, this does not mean that every technology company should make the switch. It simply means that the decision is no longer based solely on the tax burden on revenue.

Today, commercial competitiveness is also part of the equation.

Consulting and specialized services firms

Business consulting firms, engineering firms, design firms, marketing agencies, financial advisory firms, and various service providers face a similar situation.

When starting a business, staying in the Simples Nacional program is usually a natural choice.

However, as the business matures, there are some signs that indicate it is worth reviewing the framework:

- Rapid revenue growth;

- Increase in average transaction value;

- Predominance of corporate clients;

- National expansion;

- The need for stronger financial governance.

In Presumed Profit, the company can forecast its tax burden with greater stability, making financial planning and the preparation of the annual budget easier.

For CFOs, this predictability represents a significant advantage.

Commerce and Industry

Although Simples Nacional While it remains highly competitive for many commercial companies, the analysis should also take into account factors such as:

- Gross margin;

- Tax substitution;

- State tax benefits;

- Purchase volume;

- Supply chain.

Industrial companies face an even more complex landscape. In addition to federal taxation, factors such as the ICMS, regional incentives, tax credits, and supply chain planning come into play.

In many cases, remaining in the Simples Nacional program means forgoing credit recovery mechanisms that could reduce the tax cost of the transaction.

However, once again, there is no ready-made answer. There is a need to expert analysis.

When Is It Worth Switching from Simples Nacional to Presumed Profit?

The transition between systems should not occur simply because the company has grown. It should be the result of a technical study. In the CLM Controller, certain factors often set off alarm bells:

Revenue growth: Companies approaching the R$ limit of 4.8 million typically need to begin this assessment even before reaching the cap.

Waiting for the mandatory reclassification may prevent proper planning. In addition, the company misses the opportunity to compare scenarios in advance.

Primarily B2B customers: When virtually all revenue comes from other companies, the choice of tax regime can directly affect business competitiveness.

Depending on the clients' profile, a structure that allows for the most effective use of tax credits can provide an advantage in negotiations.

This aspect has become even more important with the gradual implementation of the Tax reform.

Planning for Investment Attraction: Startups and scale-ups looking to raise funds often invest in professionalizing their financial controls.

Although the tax system is not, on its own, a determining factor in an investment round, it does influence:

- Accounting organization;

- Financial predictability;

- Transparency of the financial statements;

- Quality of management information.

These factors boost the confidence of investors and financial institutions.

Tax outsourcing

The strategic solution for companies

Practical simulations: Simple vs Presumed tax

Compare Simples Nacional and Lucro Presumido requires more than looking at tax rates in tables. The tax impact varies according to the sector, the payroll, the profit margin and the company's operating model.

Below you can see real simulations based on three common profiles among companies served by the CLM Controller Accounting.

To facilitate comparison, all companies have monthly revenue of R$ 300 thousand (R$ 3.6 million per year).

1. service company (consultancy, technology, marketing agency)

Typical scenario: Company with a high profit margin, few fixed costs, lean structure and payroll below 28% of revenue.

- Annual revenue: R$ 3.6 million

- Annual payroll: R$ 900 thousand (25%)

- Annual profit margin: R$ 1.8 million (50%)

Simples Nacional (Annex V)

- As the payroll does not reach 28% in the last 12 months, the company does not benefit from the R Factor and automatically falls into Annex V.

- Considering the company's turnover and the value of the reduction factor, the effective tax rate is approximately 15.50% on turnover.

- Approximate annual tax: R$ 558.000,00

Presumed Profit

- The calculation basis for IRPJ and CSLL will be 32% billing

- Effective rates IRPJ (4.8%) + CSLL (2.88%) + PIS (0.65%) + COFINS (3%) + ISS (2%)

- Total effective tax rate: ~13.33% on turnover

- Approximate annual tax: R$ 479.880,00

AnalysisThe annual difference between the two regimes is R$ 78.120,00 which represents a monthly saving of R$ 6,510.00.

Presumed Profit offers a clear advantage for companies with a high profit margin and a lean payroll, especially in intellectual services.

Best choicePresumed Profit, with ease. In addition to savings, the system offers fiscal predictability and a better structure for growth.

2. Retail (e-commerce, physical store, market)

Typical scenario: Company with higher operating costs, lower payroll, focus on sales volume and tight profit margin.

- Annual revenue: R$ 3.6 million

- Annual payroll: R$ 720 thousand (20%)

- Annual profit margin: R$ 360 thousand (10%)

Simples Nacional (Annex I)

- Initial nominal rate: 4%

- With the advance in accumulated revenue, the effective tax rate rises to around 8.5% on turnover

- Approximate annual tax: R$ 306 thousand

Presumed Profit

- Presumption basis for IRPJ/CSLL: 8% turnover

- Effective federal tax rate: 5.93% on turnover

- Approximate monthly tax: R$ 213.5 thousand

AnalysisIn this profile, Presumed Profit initially appears to be the best option, but what will confirm this information is the percentage that ICMS costs will represent on the business's turnover and margin.

This analysis needs to be carried out individually, as each company has different volumes of purchases and sales of goods, which are subject to ICMS.

Best choiceThe precise answer depends on the ICMS tax burden faced by the business.

3. Industry (food manufacturing, cosmetics, light metallurgy)

Typical scenario: Company with production processes, moderate fixed costs, constant turnover and reasonable margins.

- Annual revenue: R$ 3.6 million

- Annual payroll: R$ 1.08 million (30%)

- Annual profit margin: R$ 720 thousand (20%)

Simples Nacional (Annex II)

- Starting rate: 4.5%

- Considering accumulated revenue, the effective tax rate rises to around 10%

- Approximate annual tax: R$ 360 thousand

Presumed Profit

- Presumption basis for IRPJ/CSLL: 8% turnover

- Effective federal tax rate: 5.93% on turnover

- Approximate monthly tax: R$ 213.5 thousand

AnalysisIn this profile, Presumed Profit also appears as the best option, but what will confirm this information is the percentage that ICMS costs will represent on the business's turnover and margin.

Best choiceThe precise answer depends on the ICMS tax burden faced by the business.

- Accounting organization;

- Financial predictability;

- Transparency of the financial statements;

- Quality of management information.

These factors boost the confidence of investors and financial institutions.

When to migrate from Simples Nacional to Lucro Presumido?

"It is compulsory to migrate from Simples Nacional to another regime when you exceed R$ 4.8 million, but it can be advantageous to change before then."

- Companies are obliged to leave Simples when they exceed R$ 4.8 million in annual turnover.

- However, in some cases, it is worth leaving earlier - especially when the Simples rates get too high or the activity proves to be more advantageous in another regime.

Having said that, and now that you're familiar with the regimes, let's look at the main signs that it's time to change. exchange Simple for Presumed Profit.

1. Turnover close to the Simples ceiling

O limit of R$ 4.8 million per year is non-negotiable. If this is exceeded, the company will be excluded from Simples the following year.

But around R$ 3.6 million a year, the effective tax rate is already close to 20%, making the regime less advantageous.

If your company is projecting growth in the coming months, it's worth doing the simulation now and considering migrating before it becomes compulsory.

2. Profit margin

Companies with high profit margins, can benefit from the Presumed Profit regime, since the percentages of presumed profit used in this regime can be lower than the presumed profit. the company's real profit.

Similarly, there are also situations where companies with very low profit margins end up being penalized by Simples.

In practice, this is because in Simples Nacional, taxes are calculated on the gross turnover, i.e. the entire business.

3. Activities not properly included in Simples

Some companies in the service sector, for example, often end up automatically falling into Annex V, which has the highest rates, among them:

- Advertising agencies

- Consulting

- Technology companies and startups

In view of this, Presumed Profit can offer a much lower tax burden, as well as greater predictability.

4. Need to highlight taxes and generate tax credits

Simples Nacional, presumed profit or simple profit which is better which prevents your customers from taking advantage of credits.

- This can make B2B sales to large companies impossible.

- It also makes it difficult to recover ICMS or PIS/COFINS credits on inputs, especially for importers or manufacturers.

In Presumed Profit, this is possible, and your company becomes more competitive.

5. Planning for growth, investment or sale of the company

Companies in Simples have restrictions on activity, partners and structure.

If you're thinking of:

- Attracting investors

- Expand to other cities

- Buying new companies

- Participate in larger tenders

It's time to professionalize your accounting and migrate to a system such as Presumed Profit or even Real Profit.

6. Other important points to consider

In addition to tax factors, the migration to Presumed Profit can represent an important milestone in the evolution of business management.

By requiring complete bookkeeping, this change forces entrepreneurs to adopt more organized practices, with greater financial control, analysis of results and a strategic vision of the business.

In practice, this facilitates decision-making, improves governance and contributes to the company's sustainable growth.

Another relevant point is access to lines of credit and financing, since banks and financial institutions tend to look favorably on companies that present complete balance sheets and consistent financial reports.

This is because Presumed Profit offers a more solid base of information for credit analysis, which can result in more attractive rates and higher limits.

Companies wishing to participate in import/export operations or close contracts with large corporations also benefit from this change.

Highlighting taxes on invoices and a robust accounting structure are often requirements in formal contracting processes.

How to migrate from Simples Nacional to Lucro Presumido?

When the strategic decision to change regime has been made, a new doubt arises: how to migrate from Simples Nacional to Lucro Presumido safely, without compromising the company's financial and fiscal health?

The transition can only take place at the beginning of the calendar year, with the last working day of January being the deadline for requesting to opt out of Simples Nacional and join Lucro Presumido.

Therefore, it is essential that planning is done in the last quarter of the previous year, with simulations, document organization and adequate technical support.

See below for a complete step-by-step guide to making the move safely:

1. Carry out a detailed tax analysis

The first step is to understand whether the switch really makes sense for your company. That's why it's essential to compare the effective tax burden of Simples Nacional with that of Lucro Presumidoconsidering:

- Monthly and annual turnover

- Operation profit margin

- Type of activity

- Incidence of taxes such as ICMS or ISS

- Whether or not tax credits can be used

Realistic simulations based on actual company data are indispensable. With this in mind, specialized accountants can use advanced tools and spreadsheets to calculate the monthly and annual tax in both regimes, enabling a technically based decision.

2. Request removal from Simples Nacional

Having confirmed that migrating to Presumed Profit is advantageous, it's time to formalize the withdrawal from Simples Nacional. This process must be done:

- Through the Simples Nacional portal, accessing with the company's digital certificate

- Until the last working day of January of the calendar year in which you wish to adopt the new regime

- With the knowledge that, once done, the disqualification is irreversible for that year

In addition, if the company issues invoices with state or municipal registration, it will also be necessary to notify the local tax authorities (SEFAZ and City Hall) of the change in tax regime.

3. Adapt the company's accounting

O Simples Nacional allows simplified bookkeeping, but by migrating to Presumed Profit, your company is now obliged to keeping more robust accountswith the following measures:

- Adoption of a chart of accounts compatible with tax requirements

- Complete bookkeeping, including ledger and general ledger

- Recording and organizing the company's tax and financial documents

- Correct calculation of IRPJ and CSLL based on legal presumptions

- Preparation of periodic balance sheets and DREs (Profit and Loss Account)

This process requires greater integration between sectors of the company (sales, finance and accounting), as well as an accountant or accounting firm with experience in more complex regimes.

4. Update systems and invoice issuers

In Presumed Profit, The taxes are not unified in a single form (DAS). For this reason, invoice issuing systems need to separate PIS, COFINS, ISS, ICMS and other taxes, depending on the activity carried out and the percentages due.

What's more:

- For some activities, ISS must be broken down by municipality

- The company may need to configure different CFOPs (Tax Codes for Transactions and Services)

- Specific tax files need to be generated, such as EFD Contributions and SPED Fiscal ICMS/IPI

If the system is not configured correctly, there is a risk of inconsistent information in tax returns, which can lead to assessments, fines and problems in relations with clients who depend on the invoice for tax credit.

5. Establish a routine for continuous accounting monitoring

Unlike Simples, where monthly calculation is relatively simple, Lucro Presumido requires greater control over ancillary obligations, such as:

- EFD Contributions (PIS and COFINS Sped)

- EFD ICMS/IPI (for companies with state registration)

- DEFIS and DIRF (when applicable)

- Correct and punctual issuance of separate forms: IRPJ, CSLL, PIS, COFINS, ISS, ICMS

It is essential to have experienced accounting adviceIt also offers ongoing consultancy, avoiding errors and identifying opportunities for legal tax savings.

Warning: poorly planned migration can lead to serious damage

- Fines for retroactive disqualification

- Loss of municipal or state tax benefits

- Operational difficulties due to lack of adaptation of systems

- Inconsistencies between accounting, invoices and declarations

So don't make this decision alone: seek the support of experts to ensure a smooth and safe transition.

Advantages and disadvantages of migration

If you are in doubt about when leaving Simples Nacional, It's worth analyzing the pros and cons based on your company's reality:

Advantages of Presumed Profit:

- Reduced tax burden for companies with high profit margins

- Highlighting of taxes on the invoice, allowing the customer to take advantage of credits

- Use of ICMS, PIS and COFINS credits when importing or purchasing taxed inputs

- More acceptance in the B2B market, especially when a tax invoice is required

- More structured accounting, which facilitates financial analysis and planning for expansion or fundraising.

Disadvantages of Presumed Profit:

- Greater accounting and tax complexity, requiring ongoing technical support

- More monthly and quarterly accessory obligations

- Need for complete and accurate bookkeeping

- Less flexibility for companies with low profit margins, which may pay more tax under the Presumed system

Comparative table: Simples Nacional x Lucro Presumido

The role of advisory accounting in this decision

A few years ago, the role of accounting was basically to calculate taxes and file related filings. Today, that role has changed completely.

Growing companies need information to support strategic decisions. It is in this context that the consultative accounting.

More than just calculating taxes, it acts as a partner to management, providing analyses that help the company grow in a sustainable way.

In terms of taxation, this means:

- Periodically review the tax framework;

- Simulate different tax scenarios;

- Monitor changes in legislation;

- Assess the impacts of the tax reform;

- Structure corporate reorganizations when necessary;

- Support decisions related to the company's expansion.

To CFOs, this type of support makes it possible to turn taxation into a source of competitiveness, rather than just a cost center.

Conclusion

Understanding When to migrate from Simples Nacional to Lucro Presumido? is essential for companies that are growing, seeking greater tax savings or preparing to expand in a structured way.

The choice of tax regime has a direct impact on business profits, management and competitiveness.

If you realize that your business:

- It's already close to the Simples ceiling,

- You're paying very high tax rates;

- It caters for companies that require a tax invoice;

- It is losing competitiveness and profit margins due to high taxes.

Perhaps now is the right time to consider tax planning, with a view to migrating from Simples Nacional to Lucro Presumido as soon as possible.

Do you want to compare your numbers (and not “guess”)?

We simulate the two regimes and show the best way to pay what is fair and gain predictability.

Talk to CLM Controller and receive a personalized analysis to pay less tax legally

Upgrade your finances:

Talk to us!

FAQ: Simples Nacional vs Lucro Presumido (2026)

What is the main difference between Simples Nacional and Lucro Presumido?

Simples Nacional unifies taxes in a single form (DAS), with variable rates depending on turnover and activity. Lucro Presumido calculates taxes separately based on fixed presumptions about turnover.

What is the turnover limit to remain in Simples Nacional?

Up to R$ 4.8 million per year, but if it exceeds R$ 3.6 million, the company loses the benefit of collecting ICMS and ISS in the DAS, which increases complexity and can impact the final amount of taxes.

Do service companies pay more with Simples or Presumido?

It depends on the payroll and the R Factor. If the payroll is small, the company can fall under Annex V and pay up to 19.5%. In these cases, Presumed Profit is usually more advantageous.

Can you change regime at any time?

No. Migration between tax regimes should generally be done at the beginning of the calendar year (by January), with exceptions (such as forced disqualification). Therefore, planning must be done in advance.

Is it worth doing full accounting for Simples Nacional?

Yes, although it is not compulsory, full accounting allows you to simulate scenarios, understand real profitability and prepare for a possible migration to Presumed or even Real Profit.

Is Presumed Profit worth it for my company?

If your company is growing, has a good profit margin and is feeling the weight of Simples Nacional taxes, it's well worth evaluating. There is no standard answer - you need to simulate both scenarios with real data.

Is it possible to return to Simples Nacional after migrating?

Yes, as long as the company meets the requirements again (turnover, type of company, permitted activities, etc.). However, the ideal is to plan the migration with a medium- and long-term vision.